As word spread about the Supreme Court’s opinion in South Dakota v. Wayfair, Inc., Dkt. No. 17-494, 485 U.S. (June 21, 2018), tax administrators around the country popped open bottles of champagne and began toasting the end of the “physical presence” substantial nexus standard. The sounds of celebration were, at least initially, particularly deafening in Louisiana, with its sixty-three (63) autonomous parish taxing jurisdictions that levy, administer and collect local sales and use tax on behalf of numerous cities, towns, districts and other local jurisdictions. Remote sellers might have considered downing a drink or two to drown their sorrows at the thought of potentially having to navigate the complex systems of state and local sales taxes in Louisiana.

As word spread about the Supreme Court’s opinion in South Dakota v. Wayfair, Inc., Dkt. No. 17-494, 485 U.S. (June 21, 2018), tax administrators around the country popped open bottles of champagne and began toasting the end of the “physical presence” substantial nexus standard. The sounds of celebration were, at least initially, particularly deafening in Louisiana, with its sixty-three (63) autonomous parish taxing jurisdictions that levy, administer and collect local sales and use tax on behalf of numerous cities, towns, districts and other local jurisdictions. Remote sellers might have considered downing a drink or two to drown their sorrows at the thought of potentially having to navigate the complex systems of state and local sales taxes in Louisiana.

As tax administrators continued to read the Wayfair opinion, however, a sobering reality began to set in that, at least in the short term, Louisiana’s various taxing jurisdictions are in no better position to force remote sellers to collect and remit state and local sales taxes than they were before the Wayfair decision (and perhaps even a worse one).

Continue Reading Not So Fast: Louisiana State and Local Sales Taxes in a Post-Wayfair World

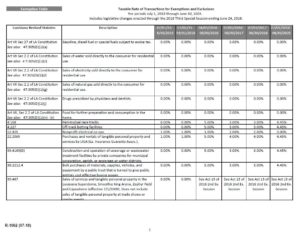

The Louisiana Department of Revenue has now issued a revised

The Louisiana Department of Revenue has now issued a revised

It’s now official. Louisiana Governor Jon Bel Edwards (D) has finally released his

It’s now official. Louisiana Governor Jon Bel Edwards (D) has finally released his  Louisiana Governor John Bel Edwards (D) recently met with leaders from the Louisiana Legislature to discuss his draft

Louisiana Governor John Bel Edwards (D) recently met with leaders from the Louisiana Legislature to discuss his draft

In response to the impact of Hurricanes Harvey and Irma, parts of the United States have been declared as major disaster areas by the federal government. As a result, numerous states have enacted delayed filing and payment periods for individuals and businesses located in these major disaster areas. Louisiana has joined this growing list with

In response to the impact of Hurricanes Harvey and Irma, parts of the United States have been declared as major disaster areas by the federal government. As a result, numerous states have enacted delayed filing and payment periods for individuals and businesses located in these major disaster areas. Louisiana has joined this growing list with