The Louisiana Department of Revenue has now issued a revised “Taxable Rate” chart (Form R-1002) to provide the Department’s understanding of the new Louisiana state-level sales/use/lease tax rates following the Louisiana legislature’s enactment of the sales tax revenue measure Act 1 (HB 10) in the recently-concluded third special session of the legislature, effective July 1, 2018.

The Louisiana Department of Revenue has now issued a revised “Taxable Rate” chart (Form R-1002) to provide the Department’s understanding of the new Louisiana state-level sales/use/lease tax rates following the Louisiana legislature’s enactment of the sales tax revenue measure Act 1 (HB 10) in the recently-concluded third special session of the legislature, effective July 1, 2018.

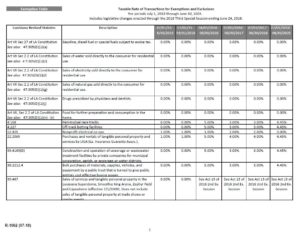

A copy of the Department’s new 21-page “Taxable Rate” chart can be found here:

http://revenue.louisiana.gov/Publications/R-1002(07-18).pdf

CAUTION: Taxpayers should be mindful that the rates noted in the new “Taxable Rate” chart represent the Department’s interpretation of the applicable rate looking at each specific exemption or exclusion separately and in a vacuum, without taking into account the potential availability of various overlapping exemptions and exclusions that may be applicable to the same type of product, service, or transaction. Also, as this chart is very new, the chart has not yet been exhaustively reviewed by practitioners and business and industry groups to determine/confirm accuracy.

These state-tax rate changes are the direct result of the highly contentious sales tax revenue measure (Act 1) that was finally agreed upon among the Louisiana legislators late last week following three special legislative sessions in 2018 alone. Act 1 was enacted to address and offset the looming “fiscal cliff” revenue shortfall that was going to take effect in Louisiana on July 1, 2018. Act 1 generates the revenue by continuing the imposition of 0.45% of the expiring 1% “clean penny” state sales tax and also imposing a temporary suspension/repeal of the availability of certain exemptions and exclusions to all 4.45% of the state sales tax as of July 1, 2018. It should also be noted that business utilities will be taxed at a lower state sales tax rate of 2% during this time period. These new changes are to be effective for 7 years and will sunset on June 30, 2025.

The state-level sales tax revenues approximated to be generated from Act 1 (per the enrolled bill’s fiscal note) are: $466 mil for the 2018-2019 fiscal year, and $502 mil for each of the 2019-2020, 2020-2021, 2021-2022, and 2022-2023 fiscal years (total of $2.474 billion over the first five years).