Jones Walker SALT partner, John Fletcher, was quoted in the article “Calif. Pork Law Fight May Guide Post-Wayfair Tax Challenges,” published by Law360 on October 14, 2022. The article covers an ongoing US Supreme Court Case regarding interstate commerce, previous tax litigation, and whether California’s importation of pork from other states violates

Jones Walker SALT partner, John Fletcher, was quoted in the article “Calif. Pork Law Fight May Guide Post-Wayfair Tax Challenges,” published by Law360 on October 14, 2022. The article covers an ongoing US Supreme Court Case regarding interstate commerce, previous tax litigation, and whether California’s importation of pork from other states violates

Addendum – Estimated Tax Payments: Mississippi Follows the National Pass-Through Entity Tax Election Trend — Start Now to Make a 2022 Tax Election

Addendum – Estimated Tax Payments: Just after our article went to press, we received some informal guidance from the DOR regarding estimated tax payments that presents a bit of a conundrum for those considering the PTE election. As explained below, it may be necessary to make duplicate estimated payments at both the entity

Mississippi Follows the National Pass-Through Entity Tax Election Trend — Start Now to Make a 2022 Tax Election

This year, a number of state legislatures considered and passed legislation that creates a pass-through entity (PTE) tax as a workaround to the $10,000 cap on the state and local tax (SALT) itemized deduction. Nearly 30 states have enacted a PTE tax. Mississippi is one of the more recent states to join the ranks.

Beginning

It’s That Time of Year Again! The Property Tax Rolls Will Soon Open For 2022 (2023 For Orleans Parish)

Like that much anticipated annual visit to the doctor before school starts, it is again time for Louisiana assessors to open their rolls for taxpayer review, and hopefully no one will need any shots afterwards (but if so, make it tequila!). Many assessors begin the two-week exposure period on August 15th, but the dates vary

John Fletcher Quoted in Law360 and TaxNotes on Mississippi Proposed Tax on Cloud Computing Services

Jones Walker SALT partner, John Fletcher, was quoted in the Law360 article “Miss. Pulls Proposed Rule To Tax Cloud Computing Services – Law360” as well as the Tax Notes article “Mississippi Revokes Proposed Sales Tax Reg for Online Computing Services.” Referring to the Mississippi Department of Revenue’s recently withdrawn rule change

Louisiana Tax Commission Sets Dates for 2023 Rules and Regulations Sessions

For anyone interested in Louisiana property tax issues, the Louisiana Tax Commission has given notice of the dates for its annual Rules and Regulations hearings. Any interested party can submit a proposal to amend the current regulations to the Commission during this process. The Commission accepts written proposals that are presented in an open Commission

Mississippi Enacts Pass-Through Entity Income Tax Election/ SALT Cap Workaround

Mississippi recently passed a SALT cap workaround in the form of a flow-through entity election. Consistent with the roughly 26 other states having adopted similar schemes, the Mississippi bill presents several grey areas and questions that will need to be addressed through Department of Revenue guidance or possible technical corrections.

H.B. 1691, signed into

Louisiana Tax Commission Issues Statewide Advisory Regarding Severe Weather Event on March 22

As we have written before, any property owner whose property has been damaged or rendered non-operational as a result of an emergency declared by the governor can seek a reduction in the value of their affected property even though January 1st has passed. See La. R. S. 47:1978.1. On March 23, 2022, Louisiana

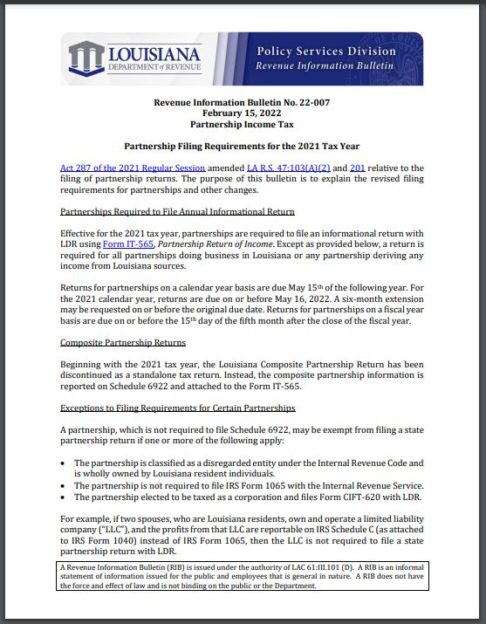

Louisiana Department of Revenue Updates Partnership Reporting Requirements

In the 2021 Louisiana Regular Legislative Session, the Louisiana Legislature enacted Act 287 making wholesale changes to the Louisiana income tax reporting and audit regime for partners and partnerships. Effective June 2021, the Act’s updated reporting obligations were made applicable to 2021 returns filed in 2022, prompting a need for guidance with respect to how

In the 2021 Louisiana Regular Legislative Session, the Louisiana Legislature enacted Act 287 making wholesale changes to the Louisiana income tax reporting and audit regime for partners and partnerships. Effective June 2021, the Act’s updated reporting obligations were made applicable to 2021 returns filed in 2022, prompting a need for guidance with respect to how

Cracking the Crypto Code: New Reporting Obligations (Current Developments in the World of Blockchain and Cryptocurrency)

As the usage of Bitcoin, Ether, and other cryptocurrencies proliferates throughout the US economy, it may seem inevitable that a comprehensive regulatory regime will sprout up around these novel assets. Thus far, the regulation has been piecemeal, primarily limited to pronouncements from the Internal Revenue Service (IRS), the Securities and Exchange Commission, and the Office