Quinn said the timing of the notice was curious because New Jersey switched to combined reporting, which requires related

Cat’s Out the Bag: First Look at the Louisiana Secretary of Revenue’s Tax Reform Plan

On July 11, 2024, the Secretary of Revenue for the State of Louisiana, Richard Nelson, briefed a joint meeting of the Louisiana House Ways and Means Committee and the Senate Revenue and Fiscal Affairs Committee on the administration’s tax proposals for a potential limited constitutional convention later this summer and the upcoming 2025 Louisiana Legislative

Big SALT Changes in the Louisiana Legislature

Unless otherwise indicated, all bills noted below have been passed by the legislature and are waiting on signature or veto by the governor. Our discussion of each bill assumes the bill is or becomes law.

SB1 by Senator R. L. Bret Allain, II

TAX/FRANCHISE/CORPORATE: Phases-out the corporate franchise tax.

SB 1 reduces the corporate franchise

New Automatic Filing Extensions for Certain Louisiana Taxpayers

In the 2022 Louisiana Regular Legislative Session, the Louisiana Legislature enacted Act 410, modifying the deadlines for filing partnership, fiduciary, and corporate income tax returns. Specifically the Act obsoleted the process by which most taxpayers obtained extensions of time to file. These changes were then implemented by the Louisiana Department of Revenue (the Department) in final

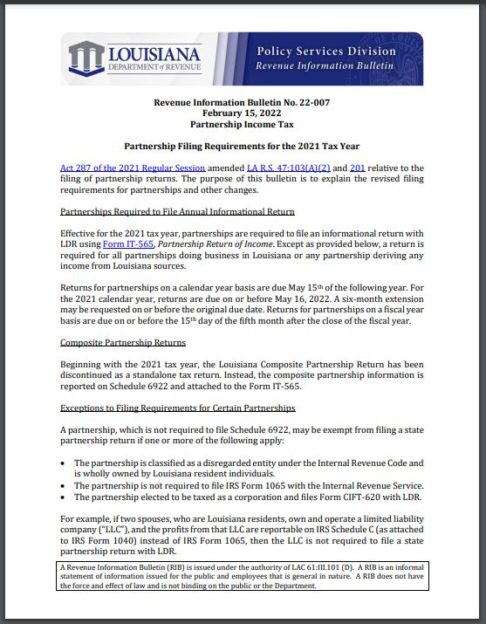

Louisiana Department of Revenue Updates Partnership Reporting Requirements

In the 2021 Louisiana Regular Legislative Session, the Louisiana Legislature enacted Act 287 making wholesale changes to the Louisiana income tax reporting and audit regime for partners and partnerships. Effective June 2021, the Act’s updated reporting obligations were made applicable to 2021 returns filed in 2022, prompting a need for guidance with respect to how

In the 2021 Louisiana Regular Legislative Session, the Louisiana Legislature enacted Act 287 making wholesale changes to the Louisiana income tax reporting and audit regime for partners and partnerships. Effective June 2021, the Act’s updated reporting obligations were made applicable to 2021 returns filed in 2022, prompting a need for guidance with respect to how

Cracking the Crypto Code: New Reporting Obligations (Current Developments in the World of Blockchain and Cryptocurrency)

As the usage of Bitcoin, Ether, and other cryptocurrencies proliferates throughout the US economy, it may seem inevitable that a comprehensive regulatory regime will sprout up around these novel assets. Thus far, the regulation has been piecemeal, primarily limited to pronouncements from the Internal Revenue Service (IRS), the Securities and Exchange Commission, and the Office