Louisiana House Bill 199, which would create a more centralized state and local sales tax collection system in Louisiana, has now been adopted by the House and Senate after negotiation in conference committee.

Louisiana House Bill 199, which would create a more centralized state and local sales tax collection system in Louisiana, has now been adopted by the House and Senate after negotiation in conference committee.

The legislative information regarding HB 199 can be found here.

The applicable conference committee report proposed by the appointed conference

Monday’s meeting in Baton Rouge of the

Monday’s meeting in Baton Rouge of the  As word spread about the Supreme Court’s opinion in

As word spread about the Supreme Court’s opinion in  The Louisiana Department of Revenue has now issued a revised

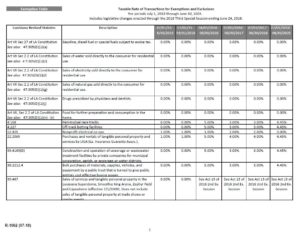

The Louisiana Department of Revenue has now issued a revised