Today, March 23, 2020, the Alabama Department of Revenue (ADOR) issued an Order in response to the COVID-19 crisis confirming that the due date for filing Alabama state Individual Income Tax or Corporate Income Tax (collectively, “State Income Tax”), Financial Institution Excise Tax (FEIT), or Business Privilege Tax (BPT) returns and making corresponding State Income

Today, March 23, 2020, the Alabama Department of Revenue (ADOR) issued an Order in response to the COVID-19 crisis confirming that the due date for filing Alabama state Individual Income Tax or Corporate Income Tax (collectively, “State Income Tax”), Financial Institution Excise Tax (FEIT), or Business Privilege Tax (BPT) returns and making corresponding State Income

Louisiana Supreme Court “Deals” a Win to Wal-Mart.com and other Online Marketplaces

Today, in a case of first impression that has captured national attention, the Louisiana Supreme Court held in a 4-3 decision that Wal-Mart.com (an online marketplace facilitator) is not required to collect and remit Jefferson Parish sales tax on behalf of its third-party sellers.

See Normand v. Wal-Mart.com USA, LLC, 2019-263 (La. 12/29/19), __

Wal-Mart.com Oral Argument at Louisiana Supreme Court Now Set for September 4th

The date and time are now set for the much-anticipated oral argument of the Wal-Mart.com “marketplace” litigation matter in Louisiana’s highest court!

On September 4th, at 2:00 PM CT, the Louisiana Supreme Court will hear oral arguments of the taxpayer, Wal-Mart.com, and the local tax collector, the Jefferson Parish Sheriff’s Office (JPSO).

A link

Louisiana’s Uniform Local Sales Tax Board Issues Adopted Regulation Regarding Uniform Voluntary Disclosure Program and Related Voluntary Disclosure Agreements (VDAs)

Louisiana’s Uniform Local Sales Tax Board (“ULSTB”) has now issued its adopted regulation at Louisiana Administrative Code (“LAC”) 72:I.105 (“Voluntary Disclosure Agreements”) regarding a uniform voluntary disclosure program and corresponding uniform voluntary disclosure agreement (VDA) for Louisiana local sales and use tax purposes. The final, adopted regulation contains the same language as the prior proposed

Louisiana Remote Seller Commission Issues Second Information Bulletin – RSIB 18-002 – Addressing Definition of “Remote Seller” and Further Guidance to Remote Sellers

The Louisiana Sales and Use Tax Commission for Remote Sellers (the “Commission”) has now officially issued its second information bulletin – Remote Sellers Information Bulletin (“RSIB”) 18-002 – which provides a general definition for “remote sellers,” as well as further administrative guidance regarding current and future registration, collection, remittance, and reporting requirements for “remote sellers.”

Not So Fast: Louisiana State and Local Sales Taxes in a Post-Wayfair World

As word spread about the Supreme Court’s opinion in South Dakota v. Wayfair, Inc., Dkt. No. 17-494, 485 U.S. (June 21, 2018), tax administrators around the country popped open bottles of champagne and began toasting the end of the “physical presence” substantial nexus standard. The sounds of celebration were, at least initially, particularly deafening in Louisiana, with its sixty-three (63) autonomous parish taxing jurisdictions that levy, administer and collect local sales and use tax on behalf of numerous cities, towns, districts and other local jurisdictions. Remote sellers might have considered downing a drink or two to drown their sorrows at the thought of potentially having to navigate the complex systems of state and local sales taxes in Louisiana.

As word spread about the Supreme Court’s opinion in South Dakota v. Wayfair, Inc., Dkt. No. 17-494, 485 U.S. (June 21, 2018), tax administrators around the country popped open bottles of champagne and began toasting the end of the “physical presence” substantial nexus standard. The sounds of celebration were, at least initially, particularly deafening in Louisiana, with its sixty-three (63) autonomous parish taxing jurisdictions that levy, administer and collect local sales and use tax on behalf of numerous cities, towns, districts and other local jurisdictions. Remote sellers might have considered downing a drink or two to drown their sorrows at the thought of potentially having to navigate the complex systems of state and local sales taxes in Louisiana.

As tax administrators continued to read the Wayfair opinion, however, a sobering reality began to set in that, at least in the short term, Louisiana’s various taxing jurisdictions are in no better position to force remote sellers to collect and remit state and local sales taxes than they were before the Wayfair decision (and perhaps even a worse one).

Continue Reading Not So Fast: Louisiana State and Local Sales Taxes in a Post-Wayfair World

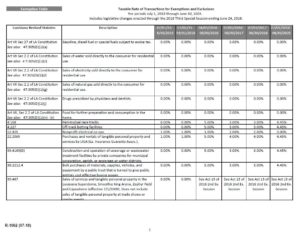

Louisiana Department of Revenue Issues New “Taxable Rate” Chart to Explain State Sales Tax Changes Following Enactment of Recent Tax Revenue Bill

The Louisiana Department of Revenue has now issued a revised “Taxable Rate” chart (Form R-1002) to provide the Department’s understanding of the new Louisiana state-level sales/use/lease tax rates following the Louisiana legislature’s enactment of the sales tax revenue measure Act 1 (HB 10) in the recently-concluded third special session of the legislature, effective July 1,

The Louisiana Department of Revenue has now issued a revised “Taxable Rate” chart (Form R-1002) to provide the Department’s understanding of the new Louisiana state-level sales/use/lease tax rates following the Louisiana legislature’s enactment of the sales tax revenue measure Act 1 (HB 10) in the recently-concluded third special session of the legislature, effective July 1,

Louisiana Governor Issues Call for Second Special Session of 2018 to Address Fiscal Cliff

Louisiana Governor John Bel Edwards (D) has now issued his anticipated call for a second special legislative session in 2018 (from May 22nd to June 4th). This 14-day special session is meant to address a stated $648 million budget shortfall, commonly known as the “fiscal cliff.” This will be the sixth special session called since

Louisiana Governor John Bel Edwards (D) has now issued his anticipated call for a second special legislative session in 2018 (from May 22nd to June 4th). This 14-day special session is meant to address a stated $648 million budget shortfall, commonly known as the “fiscal cliff.” This will be the sixth special session called since

Louisiana Governor Calls Special Legislative Session to Address Tax Issues and Looming “Fiscal Cliff”

It’s now official. Louisiana Governor Jon Bel Edwards (D) has finally released his Call for a special legislative session to begin February 19th and conclude March 7th. The Call, released today, February 9, 2018, is intended to allow the Louisiana legislature to address the long-term issue of its current taxing and spending structure, as

It’s now official. Louisiana Governor Jon Bel Edwards (D) has finally released his Call for a special legislative session to begin February 19th and conclude March 7th. The Call, released today, February 9, 2018, is intended to allow the Louisiana legislature to address the long-term issue of its current taxing and spending structure, as

Louisiana Governor Provides Draft of 2018 Tax & Budget Priorities to Address Looming Fiscal Cliff and Long-Term Tax Reform

Louisiana Governor John Bel Edwards (D) recently met with leaders from the Louisiana Legislature to discuss his draft 2018 Tax & Budget Priorities, including recommendations for how the State should address the long-term issue of its current taxing and spending structure, as well as the short-term issue of the $1 billion “fiscal cliff” looming

Louisiana Governor John Bel Edwards (D) recently met with leaders from the Louisiana Legislature to discuss his draft 2018 Tax & Budget Priorities, including recommendations for how the State should address the long-term issue of its current taxing and spending structure, as well as the short-term issue of the $1 billion “fiscal cliff” looming