Mississippi’s new direct pay permit for purchases of computer software and computer software services is now available on the Department of Revenue’s website. The Mississippi Legislature authorized this new permit earlier this year as part of the state’s comprehensive legislation on the taxation of remote software and services (see prior coverage here), which went

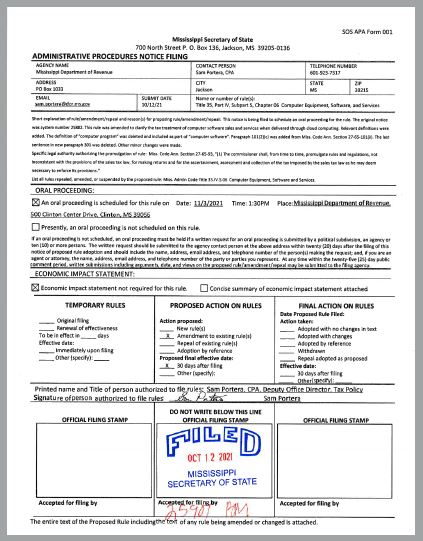

UPDATE: In response to widespread interest in these changes, the Mississippi Department of Revenue this afternoon scheduled a public hearing on the proposed amendments. The hearing is set for Wednesday, November 3 at 1:30. Interested parties are encouraged to identify specific questions and issues to present to the Department at the hearing. Jones Walker

UPDATE: In response to widespread interest in these changes, the Mississippi Department of Revenue this afternoon scheduled a public hearing on the proposed amendments. The hearing is set for Wednesday, November 3 at 1:30. Interested parties are encouraged to identify specific questions and issues to present to the Department at the hearing. Jones Walker