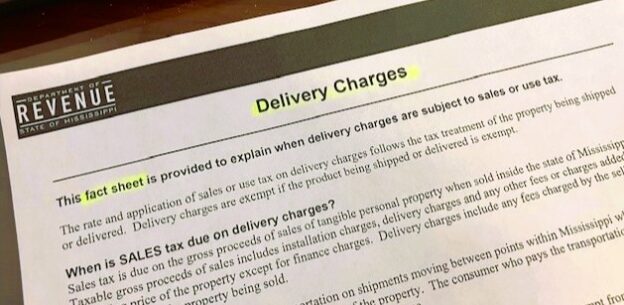

DOR “Fact Sheet” Was Not An “Other Officially Adopted Publication” And Was Not Owed Any Deference in Mississippi Tax Appeals

In an administrative tax appeal, Mississippi law requires the Board of Tax Appeals (the “BTA”) “give deference to the department’s interpretation and application of the statutes as reflected in duly enacted regulations and other officially