At the Supreme Court early with my great friend Pat Reynolds of COST. Following National Pork Producers case, will it be a sleeper SALT case? Will Pike balancing test be toast? Is the dormant Commerce Clause really a “dead letter”? Looking forward to watching my first oral arguments.

At the Supreme Court early with my great friend Pat Reynolds of COST. Following National Pork Producers case, will it be a sleeper SALT case? Will Pike balancing test be toast? Is the dormant Commerce Clause really a “dead letter”? Looking forward to watching my first oral arguments.

Addendum – Estimated Tax Payments: Mississippi Follows the National Pass-Through Entity Tax Election Trend — Start Now to Make a 2022 Tax Election

Addendum – Estimated Tax Payments: Just after our article went to press, we received some informal guidance from the DOR regarding estimated tax payments that presents a bit of a conundrum for those considering the PTE election. As explained below, it may be necessary to make duplicate estimated payments at both the entity

Mississippi Follows the National Pass-Through Entity Tax Election Trend — Start Now to Make a 2022 Tax Election

This year, a number of state legislatures considered and passed legislation that creates a pass-through entity (PTE) tax as a workaround to the $10,000 cap on the state and local tax (SALT) itemized deduction. Nearly 30 states have enacted a PTE tax. Mississippi is one of the more recent states to join the ranks.

Beginning

John Fletcher Addresses Graduates at Delta State’s 95th Commencement Ceremony

I was honored as the President of the Delta State University Alumni Association to address the new graduates at Delta State’s 95th Commencement Ceremony last Friday. Pictured with me are DSU President William LaForge and the keynote speaker, alumnus Walt Bettinger II, CEO of The Charles Schwab Corporation. Not pictured but also on stage

Mississippi Enacts Pass-Through Entity Income Tax Election/ SALT Cap Workaround

Mississippi recently passed a SALT cap workaround in the form of a flow-through entity election. Consistent with the roughly 26 other states having adopted similar schemes, the Mississippi bill presents several grey areas and questions that will need to be addressed through Department of Revenue guidance or possible technical corrections.

H.B. 1691, signed into

Mississippi Senate Counters House Proposal on Income Tax Reform

Today the Mississippi Senate released a summary of its proposal for income tax reform. Readers may recall the House passed its proposal, HB 531, and passed it on January 13 (see our prior coverage). That bill has been transmitted to the Senate and referred to the Finance Committee.

While the Senate has not yet

Mississippi House Revisits Income Tax Phase-Out for 2022

Today the Mississippi House of Representatives filed and passed out of the Ways and Means Committee H.B. 531 which appears to represent the House leadership’s income tax elimination proposal for the 2022 session. The bill, which is 294 pages long, appears to have the following primary features:

Today the Mississippi House of Representatives filed and passed out of the Ways and Means Committee H.B. 531 which appears to represent the House leadership’s income tax elimination proposal for the 2022 session. The bill, which is 294 pages long, appears to have the following primary features:

- Quantifies the amounts by which actual fiscal year

Questions Submitted for Hearing on Mississippi Software Sales Tax Regulation

In anticipation of the upcoming public hearing on Mississippi’s proposed amendments to its sales tax regulation on Computer Equipment, Software and Services, Jones Walker recently submitted a letter to the Mississippi Department of Revenue summarizing a wide range of questions and issues raised by the proposal. These questions were compiled as a result of discussions

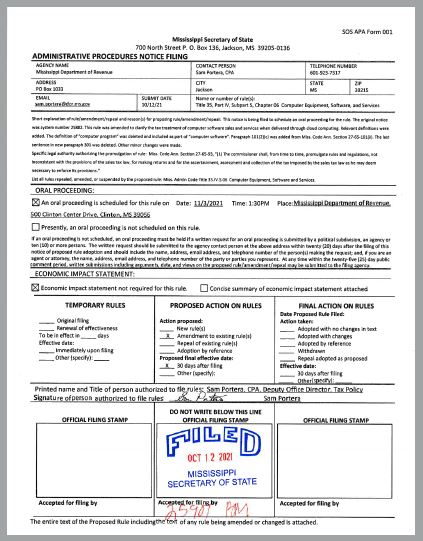

UPDATE: Mississippi Attempts to Significantly Increase Sales and Use Taxes on Internet-Based Business Services Via Regulatory Amendment

UPDATE: In response to widespread interest in these changes, the Mississippi Department of Revenue this afternoon scheduled a public hearing on the proposed amendments. The hearing is set for Wednesday, November 3 at 1:30. Interested parties are encouraged to identify specific questions and issues to present to the Department at the hearing. Jones Walker

UPDATE: In response to widespread interest in these changes, the Mississippi Department of Revenue this afternoon scheduled a public hearing on the proposed amendments. The hearing is set for Wednesday, November 3 at 1:30. Interested parties are encouraged to identify specific questions and issues to present to the Department at the hearing. Jones Walker

Mississippi Attempts to Significantly Increase Sales and Use Taxes on Internet-Based Business Services Via Regulatory Amendment

On September 24, the Mississippi Department of Revenue filed a proposed amendment to its sales tax regulation on Computer Equipment, Software and Services. This amendment appears to reverse longstanding sales and use tax policy with respect to remote internet-based computer services, and could result in a significant non-legislative tax increase on Mississippi businesses. The notice